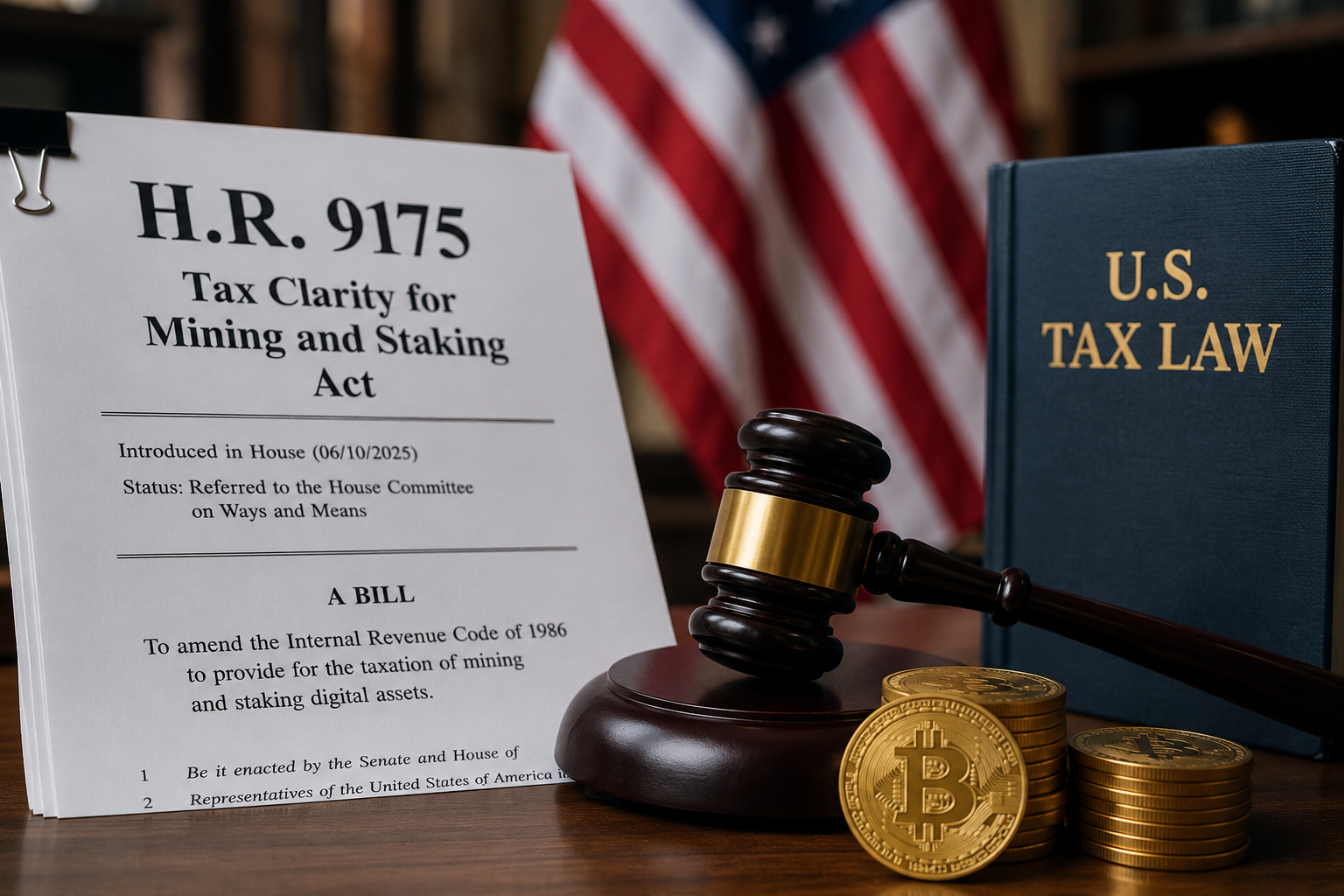

U.S. Mining Tax Bill Brings Miner Cash Flow Into the Open

Bitcoin mining policy is usually framed around electricity.

Power demand. Grid pressure. Data centers. Noise complaints. Industrial miners chasing cheaper energy. Politicians debating whether proof-of-work is productive, wasteful, or something in between.

Tax law rarely gets the same attention.

That is what makes H.R. 9175, the Tax Clarity for Mining and Staking Act, worth watching. It is not a subsidy for miners. It does not make mining tax-free. It does not improve a miner’s odds of finding a block.

The bill is about something more practical: timing.

For miners, timing is not an accounting detail. It is a cash-flow issue.

A miner can receive newly created digital assets before selling them. The asset may rise or fall sharply after receipt. Meanwhile, power bills, hardware costs, repairs, hosting fees, and operating expenses are usually paid in fiat.

That mismatch sits at the center of the tax debate.

The Bill Is Really About Timing

Under existing IRS guidance, virtual currency received through successful mining is generally included in gross income at its fair market value when received. Similar logic has also been applied to staking rewards when a taxpayer gains control over them.

That treatment may sound straightforward on paper. In practice, miners understand the problem immediately.

Receiving an asset is not the same as monetizing it.

A miner may hold the BTC. The market price may change. The miner may not want to sell. But if income is recognized at receipt, the tax obligation can arrive before the miner has converted anything into cash.

That creates pressure.

It can push miners toward selling earlier than planned simply to meet a tax liability. For a large operator, that becomes a treasury management problem. For a smaller miner, it can become a confusing and frustrating compliance problem.

H.R. 9175 tries to address that gap by creating a clearer framework for digital assets received through mining and staking. The key point is not whether rewards are taxable. The key point is when income should be recognized.

That distinction is where the bill matters.

Mining Costs Arrive Before the Tax Debate

Bitcoin mining is often reduced to a few public numbers: hashrate, block reward, power draw, network difficulty, or market price.

Those numbers matter, but they do not capture the full operating reality.

Mining starts with cost.

A miner buys hardware before earning anything. Electricity is paid continuously. Cooling and uptime matter. Hardware reliability matters. Network difficulty changes whether the same machine is producing the same expected result over time.

For industrial miners, those costs show up in financing, power contracts, fleet management, and balance-sheet planning.

For home miners, the numbers are smaller, but the logic is still real. A compact miner on a desk may not look like a mining farm, but it is still performing proof-of-work. It still consumes electricity. It still depends on stable operation. It still connects a user to the economics of Bitcoin mining in a physical way.

That is why tax timing is not only a concern for public mining companies.

It also belongs in the conversation around home mining.

Small Miners Are Part of the Same System

A Bitaxe user running a small miner at home is usually not thinking like a corporate treasury department.

The motivation may be education. It may be open-source hardware. It may be solo mining. It may simply be the desire to understand proof-of-work by running a real machine instead of reading about one.

But the moment a person runs mining hardware, the activity stops being purely theoretical.

The miner is not simulating hashes. It is not displaying fake numbers. It is doing actual work on a real network. That means the surrounding issues eventually become real as well: rewards, records, costs, reporting, and tax treatment.

That does not mean every home miner needs to become a tax expert.

It does mean clearer rules matter.

Accessible mining is not only about smaller devices and lower power consumption. It is also about whether ordinary participants can understand the obligations that come with participating.

That is the underappreciated part of this bill.

It moves the discussion beyond whether mining is profitable today and toward how mining should be treated as an ongoing economic activity.

Mining and Staking Belong in the Same Tax Debate, Not the Same Technical Box

The bill covers both mining and staking, but the two should not be blurred together.

Bitcoin mining is proof-of-work. It relies on specialized hardware performing SHA-256 hashing. Miners compete to find valid blocks and secure the network through energy-backed computation.

Staking belongs to proof-of-stake systems. Validators commit assets and participate in block validation under a different security model.

The tax debate overlaps because both activities can produce newly created digital assets through network validation. The technical mechanisms, however, are not the same.

For SoloBitaxe readers, the mining side is the important part.

The bill matters because lawmakers are trying to decide how digital assets created through validation should be handled for tax purposes. That framework could shape how miners think about rewards, holding periods, recordkeeping, and operating costs.

It is a policy issue with technical consequences.

This Is Not Current Law

The most important caveat is also the simplest one: H.R. 9175 is still proposed legislation.

Miners should not treat it as if the rules have already changed. Until a bill is passed and any required Treasury or IRS guidance is issued, existing guidance remains the practical reference point.

That caveat matters because crypto headlines often turn proposals into certainty.

This is not certainty.

It is also not personal tax advice. Miners operating in the United States should speak with a qualified tax professional about their own situation, especially if they mine as a business, hold mined assets, or have meaningful expenses connected to mining activity.

For miners outside the United States, the bill is still useful as a policy signal. It does not directly determine local tax obligations.

Mining Policy Is Getting More Serious

The strongest reason to follow this bill is not that it sounds bullish for mining.

The stronger reason is that it treats mining like a serious economic activity.

Mining is hardware, electricity, software, capital, risk, accounting, and compliance. A mature mining ecosystem needs more than efficient chips and better firmware. It also needs rules that participants can understand.

For large miners, unclear tax treatment complicates planning.

For small miners, it creates uncertainty.

For home miners, it reinforces an important point: mining is not just a hobby screen with moving numbers. It is a real connection to Bitcoin’s proof-of-work layer.

That is where this story connects naturally to Bitaxe and home mining.

A small miner does not turn someone into a mining company. But it does give that person a direct entry point into the network. It makes Bitcoin mining visible, measurable, and physical.

Once someone crosses that line, the surrounding rules start to matter.

Not because every small miner expects to find a block.

Not because every home miner is chasing income.

Because real participation comes with real context.

The Point for Bitcoin Miners

The headline is tax.

The issue underneath is cash flow.

H.R. 9175 matters because it asks a practical question: should newly created digital assets trigger income recognition before a miner or validator has actually monetized them, or should tax treatment better reflect the moment those assets are disposed of?

That question sounds technical, but miners understand the stakes quickly.

Timing affects planning. Planning affects liquidity. Liquidity affects whether mining remains sustainable.

The bill may change as it moves through Congress. It may not pass in its current form. Implementation details may still need further guidance.

Even so, the debate is important.

It shows that mining policy is expanding beyond power grids, emissions, and industrial data centers. It is beginning to deal with the basic economic reality of proof-of-work.

Bitcoin mining uses real machines, real energy, and real capital.

Tax law is now being asked to recognize that more clearly.